![]()

How families really pay for senior care, and why so many feel unprepared

Paying for senior care is a complex financial responsibility, and many families begin the process believing they understand the costs and have a plan to cover them. But once care begins, that confidence often breaks down as the full scope and variability of costs become clear.

This A Place for Mom report examines why families ultimately feel unprepared, the gap between what they expect to pay and what care actually costs, as well as the funding sources they ultimately rely on. It is based on findings from a December 2025 survey of 820 family caregivers — including those who have made a care decision for a senior loved one in the past 12 months and those who are currently searching for senior care or will soon be considering it.

Having a plan does not mean being prepared to pay for care

Confidence in a financial plan to pay for professional senior care is not the same as being prepared to cover those costs over time. More than three-quarters of family caregivers considering senior care say they are familiar with the costs of senior living and home care in their area, and nearly all report that they have a financial plan to pay for this care.

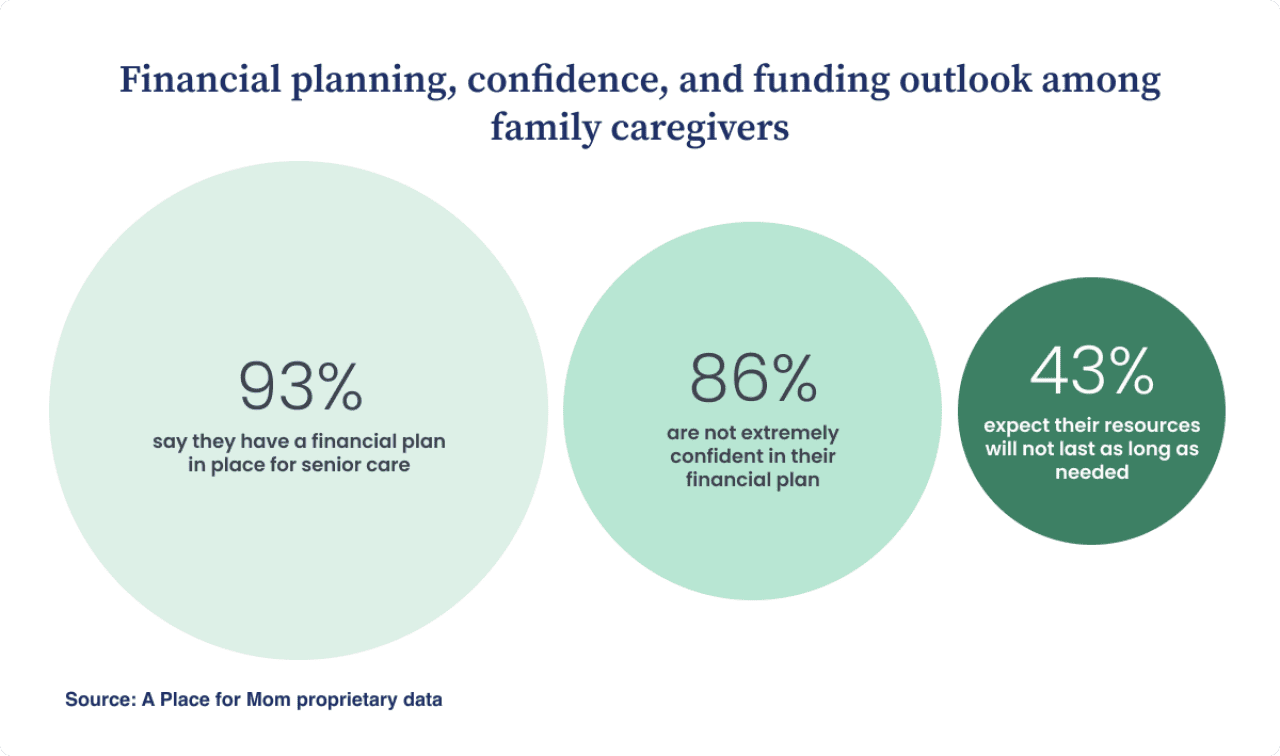

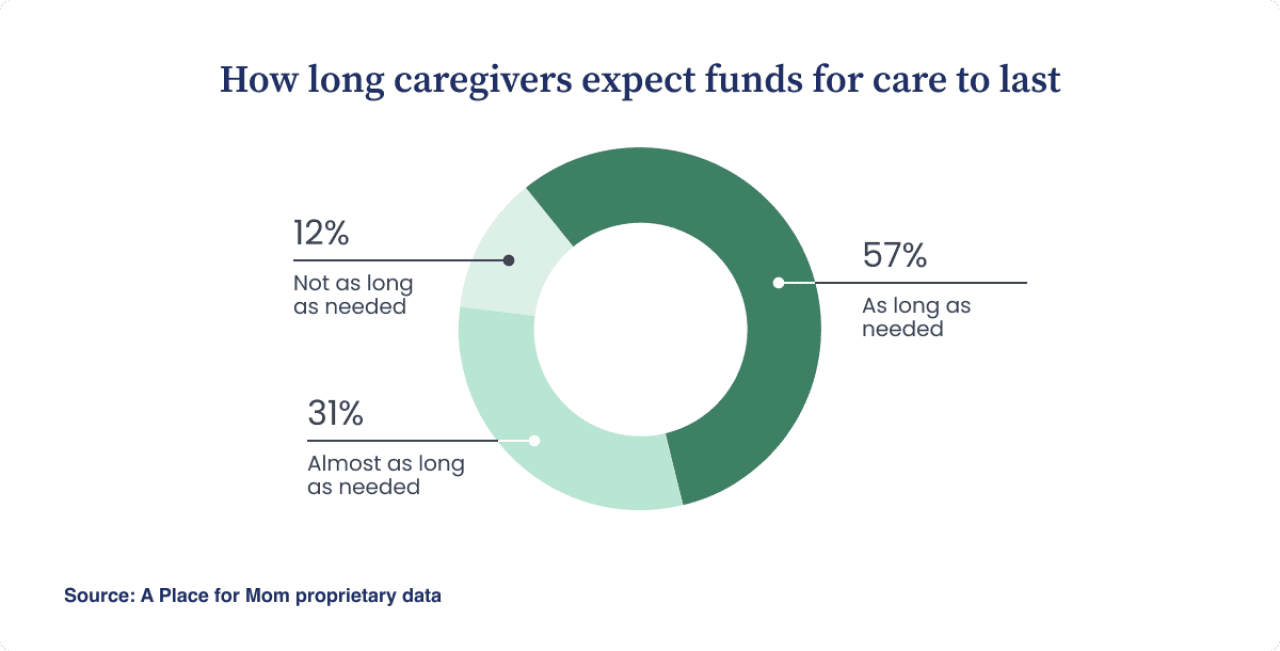

But once families secure care for their loved one, their confidence declines. Long-term care requires sustained financial planning, but because the duration of care is uncertain and care needs change, 43% of families are not confident their finances will last as long as needed.

The true cost of senior care is more complex than families expect

On average, families expect to pay approximately $3,062 per month for professional senior care. However, the actual average monthly cost of senior living is $3,816, which is 25% more than expected — a gap that becomes more apparent once families move from planning to paying. Nearly all caregivers report encountering at least one unexpected cost after care begins, from annual price increases to higher costs as care needs evolve. This disconnect between expected and actual costs is a key reason many families wind up feeling unprepared.

Funding sources are not well understood and often change over time

Families typically rely on a mix of funding sources to pay for professional care. Among caregivers who have made a care decision, 46% use their loved one’s Social Security benefits, and 42% draw from their loved one’s savings or checking accounts.

However, families often overestimate how far these sources will go. As care needs change and costs increase over time, funding plans frequently shift — requiring additional contributions, new funding sources, or greater out-of-pocket spending than originally expected.

Together, these findings show that while families believe they have a plan to pay for senior care, they often are unprepared for the true costs once care begins.

Do families feel prepared to pay for senior care?

A large majority of families (93%) have a plan for paying for senior care, but only 14% say they are extremely confident in their plan. Because both the duration and type of care can change over time, families often lack a clear sense of how long their financial resources will realistically last.

Although many families say they feel prepared and understand the costs involved, that confidence often fades once they encounter the actual costs of home care or senior living. Caregivers who have already made care decisions are less likely to say they were familiar with costs beforehand, suggesting a steeper learning curve than expected. This gap is especially pronounced for senior living, where familiarity with costs drops from 78% to 69% once families move a loved one into a community.

When Steve Michnik, 59, helped move his aunt, Sharon, into an assisted living community in Cheyenne, Wyoming, he and his family believed they had a clear financial plan. Michnik’s aunt had been diagnosed with dementia and was declining for several years, which gave them time to consider where she could live and what was affordable. Michnik’s father also had the power of attorney to see the plan through. Assisted living with a surcharge for dementia care services totaled about $10,000 per month. Michnik calculated that his aunt’s resources would cover her care for about eight years.

But within two years, his aunt’s needs increased dramatically. She had to move into a skilled nursing facility, which was even more expensive. After researching three facilities, he and his family chose one they felt could provide the best care.

“The cost went up to about $14,000 a month,” Michnik recalls.

Even well-planned finances can fall short as care needs change

Paying for care creates a meaningful financial strain for many families. More than half (64%) report that it is extremely or somewhat stressful. This strain is especially pronounced among younger caregivers, who are more likely to be balancing work, child care, caregiving responsibilities, and financial obligations at the same time. Most caregivers who are in their 40s (71%) find handling the financial aspect of senior care stressful, while only 61% of those in their 50s and 57% of those who are aged 60 to 75 report feeling this stress.

Most families facing the need for professional care regret not planning for the costs earlier. A full three-quarters say they wish they or their senior loved one had begun planning before care was needed.

Why senior care costs are higher and more complex than expected

The cost of professional senior care is shaped by complex pricing structures that make it more variable and harder to predict than families expect. On average, families expect to pay about $3,062 per month for senior care, but they find that actual senior living costs are 25% higher — a difference that often becomes clear only after care begins.

As families move from exploring options to committing, they encounter expenses they did not initially account for, from ongoing price increases to services not included in base rates. Nearly all families who chose senior living (97%) and a large majority who hired home care (83%) report encountering at least one unexpected cost.

Costs increase as care needs evolve

As a person ages, their needs naturally increase. Among families who chose senior living for their loved one, 30% were surprised to pay for supplies such as bed pads and adult diapers when the senior needed them. Similarly, when assistance with bathing, dressing, and toileting became necessary, 30% of families were surprised at having to pay for that help.

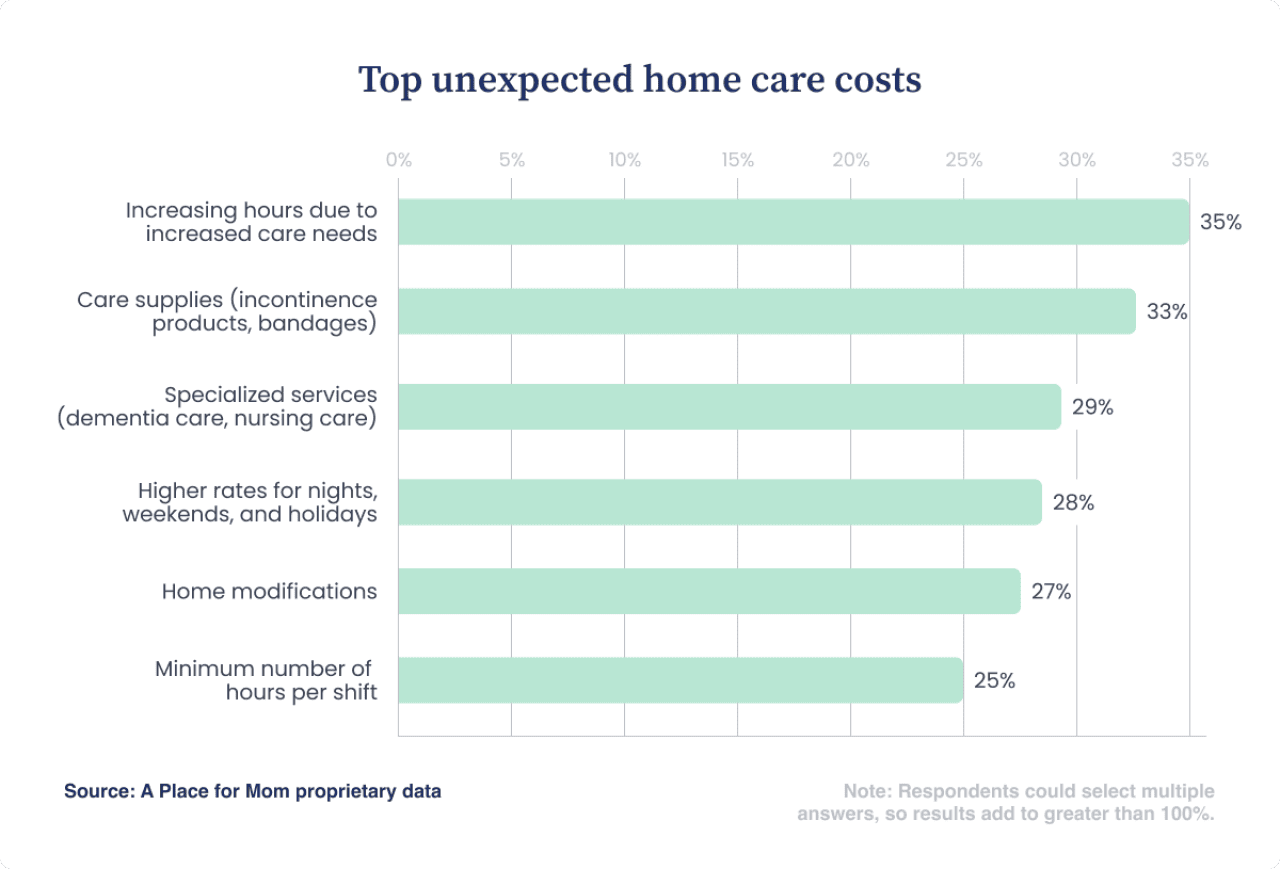

A similar pattern emerges among those who hired home care for a loved one. More than one-third (35%) were surprised by the need to increase care hours over time. A comparable share (33%) did not anticipate the ongoing cost of supplies. In addition, 29% were surprised by the cost of specialized care services, such as dementia care, Hoyer lift assistance, and post-surgical support, and 27% did not expect to pay for home modifications like bathroom remodeling or wheelchair ramps.

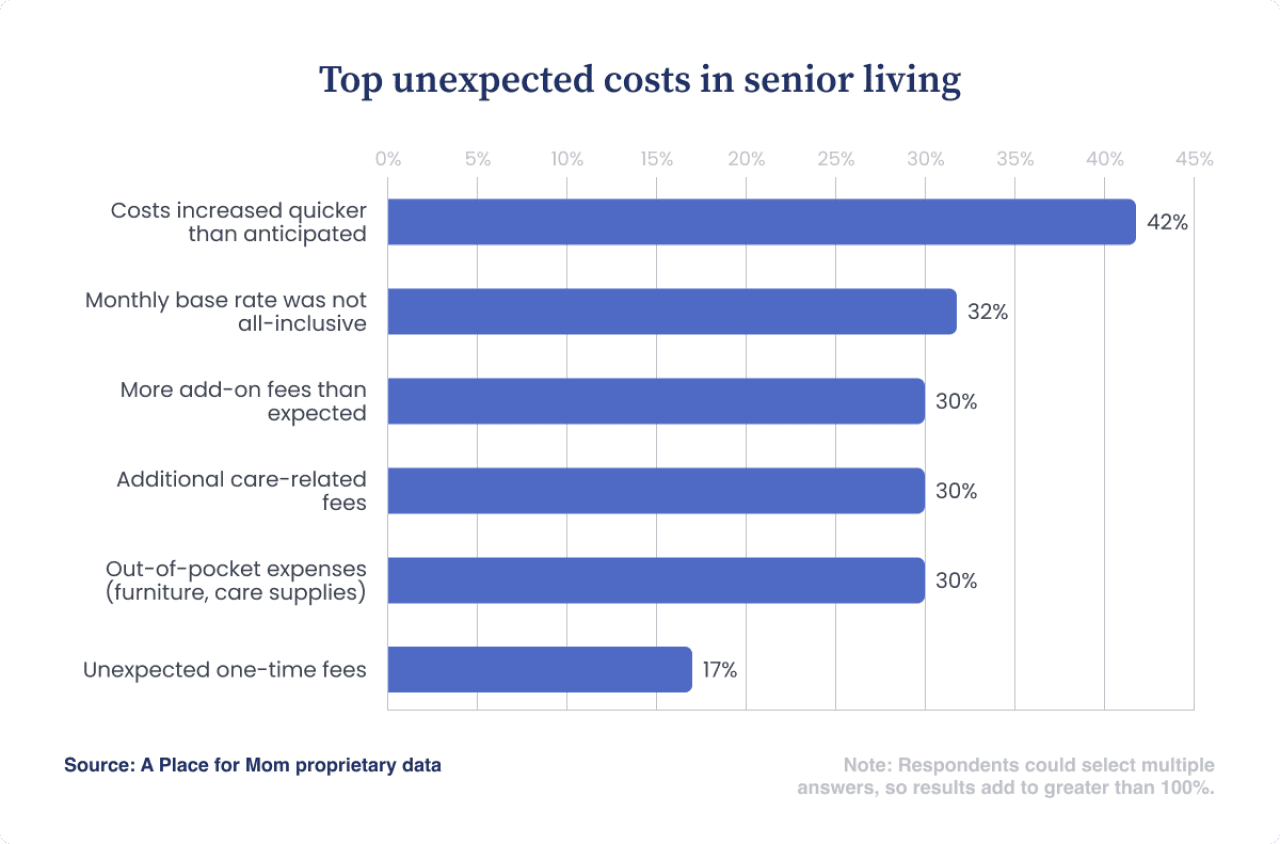

Base rates do not always reflect the total cost

A base rate is simply that — it does not include the cost of extra products or services. About one-third of families who opted for senior living reported that the base rent did not cover items they thought would be included. Another third of survey respondents found that services such as laundry and transportation came with unexpected a la carte fees. And having to buy furniture and household supplies was unexpected for 30% of families.

Michnik says there were expenses he hadn’t thought of before moving his aunt, such as furnishing her new living space. In some communities, units come furnished, while others do not — one example of how policies can vary and make total costs harder to predict.

Pricing structures vary more than families expect

Pricing for professional senior living often includes initial, typically one-time fees that are separate from the base rate, such as a security deposit, entrance fee, or move-in fee. These costs were a surprise for 17% of families. In addition, many costs increase on an annual or more frequent basis, and these came as a surprise to nearly half (42%) of families.

Home care pricing structures can also vary. Minimum hourly requirements (25%) and higher rates for nights, weekends, and holidays (28%) can increase total costs beyond what families expect.

How do families really pay for senior care?

Families typically pay for senior care using a mix of income sources such as Social Security benefits, personal savings, and contributions from family members. In practice, however, covering the cost of care often requires a more complex and shifting combination of these sources than expected.

Anticipated vs. actual funding sources

Before they understand the actual fees involved, families often overestimate how much certain funding sources will contribute to the cost of care. The largest gap appears in plans to cover costs with Social Security benefits. More than half (61%) of caregivers surveyed anticipate paying for senior care with Social Security retirement benefits or Supplemental Security Income (SSI) benefits, but in reality, only 46% could rely on those benefits. Similarly, while 46% expect to use their care recipient’s personal savings, only 42% actually do. This suggests families may overestimate how far fixed income sources will stretch once care begins.

Selling a home is another potential way to cover the costs of senior care, and 18% of families expect to use this option, but only 9% choose to do so to pay for senior care.

Many families also expect Medicare to cover a significant portion of care costs. However, Medicare does not cover long-term care and only pays for limited, medically necessary services under specific conditions. As a result, 46% of families considering senior care expect to use Medicare, but only 37% of those who have made a care decision report actually using it.

For many families, this gap between expected and actual funding sources becomes clear as they begin piecing together how to pay for care. Michnik and his family experienced this firsthand as they worked to cover the cost of his aunt Sharon’s care.

“We looked at her finances,” Michnik says. “She was a retired primary school teacher and had Social Security, which was $2,300 a month, and a pension, which was about $3,000 a month, but that only covered about half of the bill. The remainder came from her retirement investments, which were about $300,000.”

Michnik’s family was able to sell his aunt Sharon’s house — which she owned outright — as well as its contents for about $350,000. This helped extend how long her care could be covered in assisted living and then in a skilled nursing facility.

Family involvement in paying for professional senior care

Most family caregivers expect to be financially involved in paying for their loved one’s care — and in reality, nearly all are. A large portion — 88% — of family caregivers expect to directly contribute to the cost and/or help manage their loved one’s finances. A similar portion of caregivers (86%) who have made a care decision is actually involved in this capacity.

About 39% of families expect to pay for senior care with at least some of their own money, and of those who do, their financial involvement is significant. Monthly contributions vary widely, but many families are paying thousands of dollars out of pocket. On average, family caregivers spend $3,241 per month of their own money on their loved one’s care. Even when families expect to be involved, they may underestimate how much they will need to contribute and how many funding sources will be required.

Do caregivers feel confident in their ability to pay for senior care?

Most family caregivers (76%) who are searching for professional senior care say they feel at least somewhat confident in their financial plan. However, this confidence is often limited, with only 14% saying they are extremely confident in their plan and 17% reporting they are not very or not at all confident.

That confidence often looks different in hindsight. Looking back, 15% of families who have made a care decision for their loved one say they were extremely well prepared for the costs and how they would pay for them, and 27% say they were not very or not at all prepared.

Confidence also weakens when caregivers consider how long their financial resources will last. Among those already paying for care, 43% do not expect their resources to fully cover costs for as long as needed.

Ultimately, confidence in a financial plan does not always reflect how well that plan will hold up over time.

How do families adjust to financial pressure from senior care costs?

Families who anticipate or experience financial pressure from paying for a senior loved one’s care often adjust care plans or trade off services.

One immediate adjustment is choosing in-home care instead of senior living, with about 30% of families saying they would take that approach. About 25% say they would delay a move to senior living to manage costs, and a similar share says they would move their loved one into their own home to delay care expenses.

These adjustments often follow a progression from delaying or changing care decisions to reducing services once care begins.

Families delay or change care decisions to manage costs

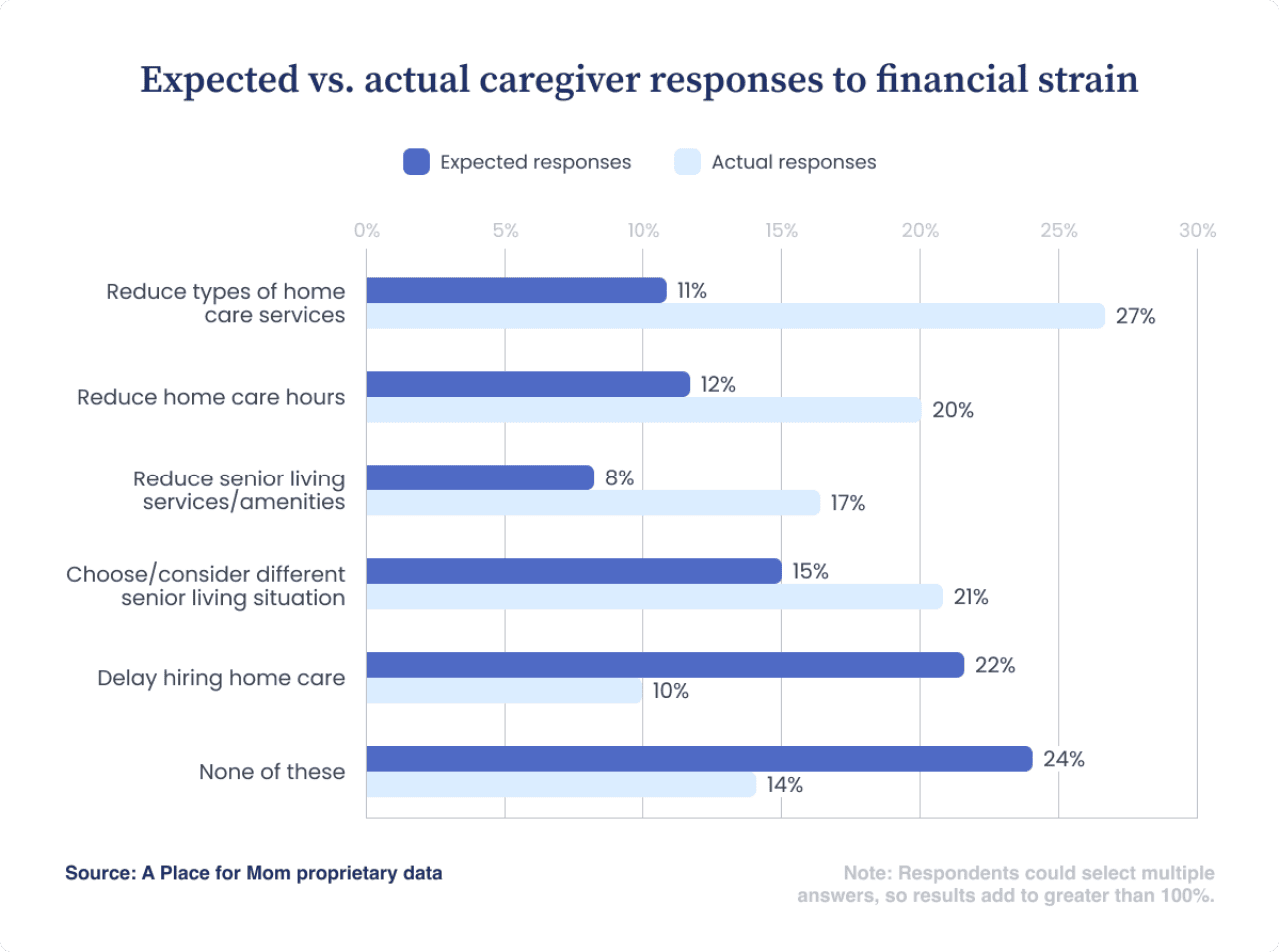

Among families who have already made a care decision, 21% say they would consider a different living situation than originally planned — such as a smaller room or a shared room — to reduce costs. By comparison, 15% of caregivers still in the planning stage say they would consider making that kind of adjustment.

A similar gap appears when it comes to delaying care. Among those still considering senior care, 22% say they would delay hiring in-home care to manage costs. In practice, only 10% of families who have already begun care say they would take that approach, suggesting that delaying care is less viable once needs become immediate.

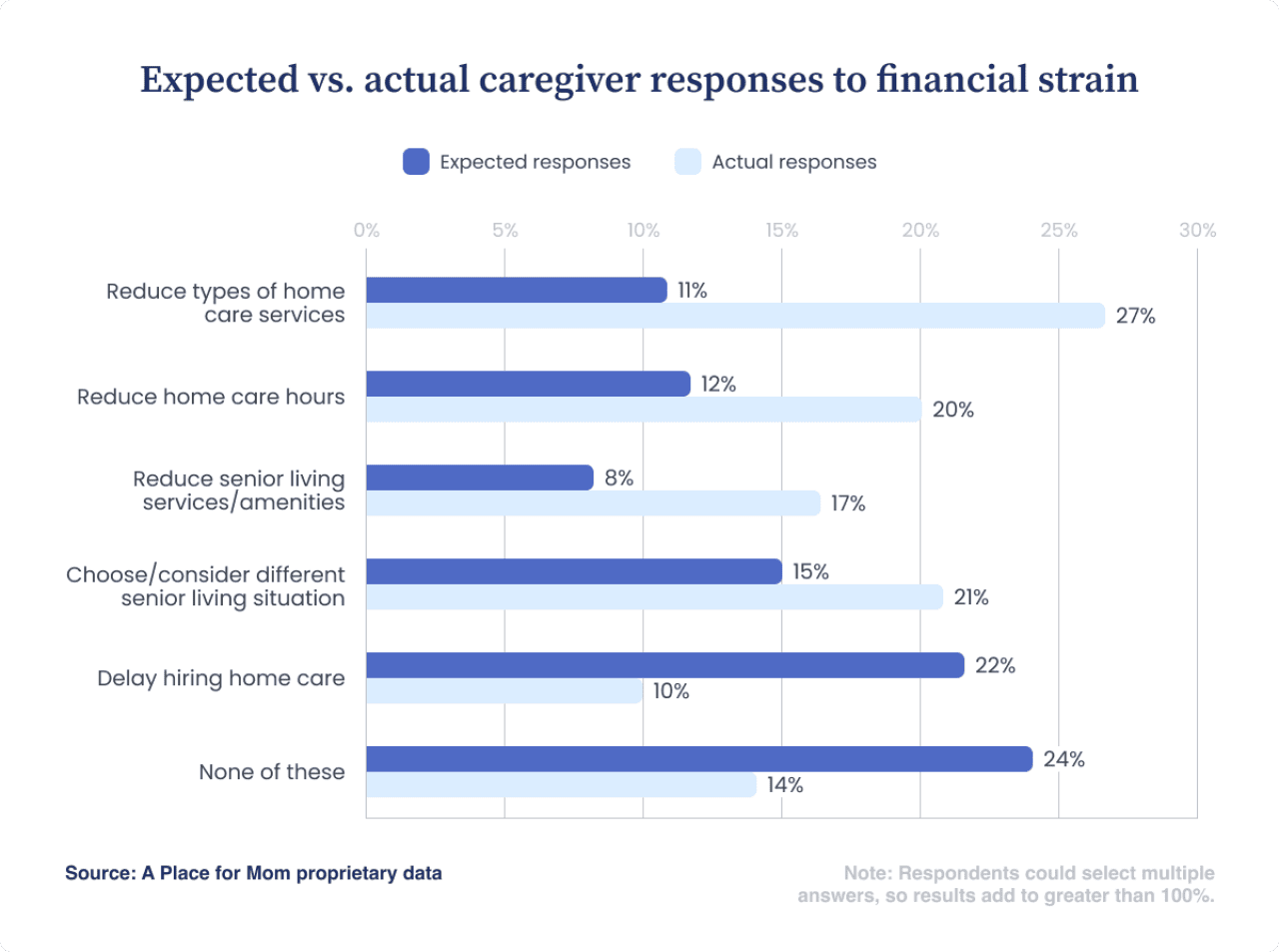

Once care begins, families are more likely to reduce services and support

Once families begin paying for care, trade-offs often shift from delaying decisions to reducing the level of care itself — a change that becomes clear when comparing expectations with actual behavior.

For example, just 8% of families in the search phase say they would cut back on amenities in senior living to manage costs, compared with 17% of those already paying for care.

A similar pattern appears in home care. Among families still searching, 11% say they would reduce services, and 12% would reduce hours. Among those already paying for in-home care, those shares more than double — 27% say they would reduce services, and 20% would reduce hours.

How can families feel more prepared for senior care costs?

Families often benefit from starting senior care conversations with clearer information about costs and payment options. Understanding pricing structures for various care types, how different funding sources contribute, and how care needs can change over time can make these discussions more productive and less overwhelming.

Many caregivers are open to planning for senior care, but uncertainty about what care will cost and how to approach the conversation often delays those discussions. Among families searching for senior care, 56% say they have talked with their loved one about how to cover costs, but at least 40% have not.

For many, the barriers are timing and clarity, not just reluctance. More than one-third (34%) say they have not had the conversation because they did not think it was necessary yet, and 23% say their loved one was unwilling to discuss it.

Without clear expectations about costs and funding, it can be difficult for families to know when or how to start planning. Conversations that happen earlier — and with a more realistic understanding of how care is paid for — can help families make more informed decisions before care becomes urgent.

Resources that break down the cost of care, explain payment options like Medicare and Medicaid, and outline common financial planning steps can help families move from general awareness to more realistic preparation.

Methodology

This report is based on the results of an online quantitative survey commissioned by A Place for Mom and conducted by Morning Light Strategy in December 2025. The study included feedback from 820 nonprofessional caregivers who care for adults aged 65 and older across the United States. Respondents include 161 people who have moved their care recipient into senior living and/or hired in-home care for their care recipient in the past 12 months, as well as 659 people who have not yet made a senior care decision.

FAQs

How do most families pay for senior care?

Most families pay for senior care using a mix of Social Security benefits, personal savings, and family contributions. Research shows programs like Medicare are often expected to cover more than they actually do, leading to funding gaps.

Why do families underestimate the cost of senior care?

Families underestimate senior care costs because pricing is complex and changes over time. Base costs often exclude additional services, rising care needs, and annual increases, which raise the total expense.

Does Medicare pay for long-term senior care?

Medicare does not cover long-term senior care. It may pay for short-term skilled care or rehabilitation, but most ongoing care — whether at home or in senior living — is paid for using personal funds or other sources.

How much do adult children contribute to senior care costs?

Among those who contribute financially, adult children spend an average of $3,241 per month on their aging parents’ senior care. Even those who do not pay directly are usually involved in managing finances and coordinating how care is funded.

Why do families feel unprepared for senior care costs?

Families feel unprepared for senior care costs because having a plan does not always mean knowing how long funds will last. Uncertainty around pricing, funding sources, and future care needs makes financial planning difficult.

When should families start planning for senior care costs?

Families should start planning for senior care costs as early as possible, ideally before care is urgently needed. Early financial planning helps set realistic expectations, identify funding options, and avoid surprises later.

This story was produced by A Place for Mom and reviewed and distributed by Stacker.

(0) comments

Welcome to the discussion.

Log In

Keep it Clean. Please avoid obscene, vulgar, lewd, racist or sexually-oriented language.

PLEASE TURN OFF YOUR CAPS LOCK.

Don't Threaten. Threats of harming another person will not be tolerated.

Be Truthful. Don't knowingly lie about anyone or anything.

Be Nice. No racism, sexism or any sort of -ism that is degrading to another person.

Be Proactive. Use the 'Report' link on each comment to let us know of abusive posts.

Share with Us. We'd love to hear eyewitness accounts, the history behind an article.