Higher gas prices are adding to the affordability crisis. This could make EVs a more attractive option for cost-conscious drivers. Sales of used EVs rose 54% in March over the previous month, according to Cox Automotive. While EVs remain more affordable to power, they’re 42% more expensive to insure than gas-powered cars, according to an analysis of Insurify’s database of more than 235 million quotes.

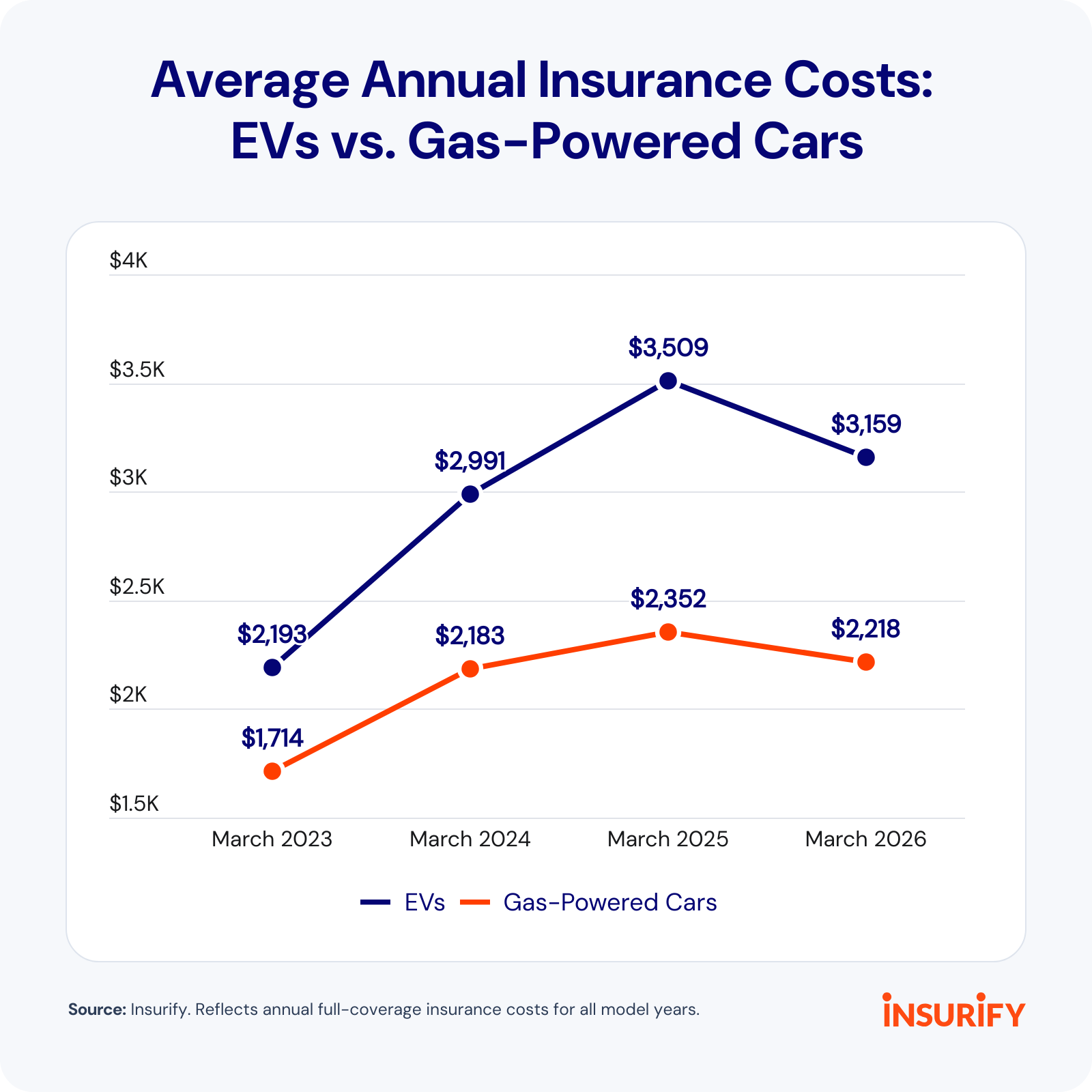

In 2026, EVs cost an average of $3,159 per year to insure with full coverage across all model years, Insurify data shows. Gas-powered cars cost $2,218 per year on average to insure. Tesla maintains the single largest share of EV sales nationwide, but its models also rank among the most expensive to insure.

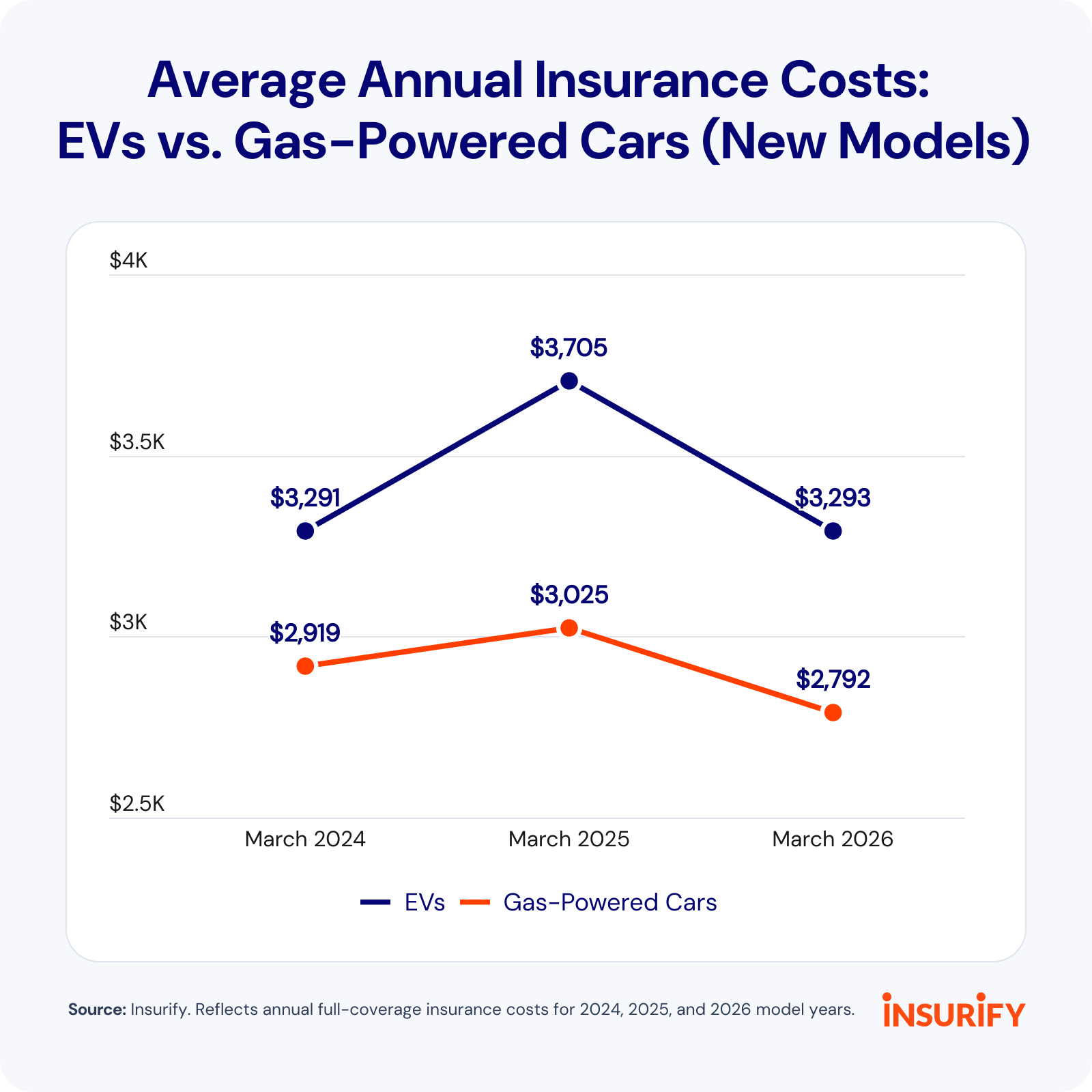

EVs often cost more to insure because they cost more to repair. Many older gas-powered cars with less technology are still on the road, contributing to that cost gap. The median vehicle age in Insurify’s database is 11.5 years. But the EV cost gap shrinks to 18% when comparing newer models (model year 2024 or newer). Broad industry adoption of assistive technology across newer vehicles is narrowing the insurance cost gap.

EV insurance costs for newer models increased 37.6% from 2023, 24% faster than insurance costs for gas-powered cars, Insurify data shows. But now EV insurance costs are going down faster than costs for newer gas-powered cars. Over the last year, average insurance rates for newer EVs dropped by 11.1%, compared with 7.7% for newer gas-powered cars. Overall, average auto insurance rates went down about 6% in 2025, according to Insurify’s auto report.

Adoption is still a moving target, however. EV sales spiked in late summer of 2025 before the federal tax credit for EV purchases ended on Sept. 30, but year-over-year sales dropped significantly following its expiration.

Now, a new bill could add to the cost of EV ownership. Because EVs don’t use gas, drivers don’t pay the federal gas tax, which supports the national Highway Trust Fund. The proposed bill would add a $130 yearly registration fee for EVs.

Proponents of the bill claim it will make sure all highway users pay their share into the fund. Under this new bill, EV owners could pay significantly more than the equivalent federal gas tax, which currently costs 18.4 cents per gallon, or $73–$89 annually, according to ZETA.

Despite the expiration of the tax credit and the proposed highway tax bill, the narrowing insurance cost gap means the annual cost of EV ownership is becoming less burdensome. Additionally, pressure at the pump is adding to greater fuel savings for EV owners. The average price of gas rose 53% from the week before the beginning of the Iran war to the end of May ($2.94 to $4.49 per gallon). Higher gas prices could mean EV owners will save an estimated $1,508 per year in fuel costs.

Some areas of the country face more of an insurance cost gap than others. Auto insurance rates, as well as EV adoption and infrastructure, vary significantly by location, contributing to regional differences. The insurance cost gap is highest in New York and New England, particularly in Massachusetts and Rhode Island, largely due to dense urban exposure.

Key findings

The average annual cost of insuring an EV is $3,159, about 42% ($941 annually) higher than insuring a gas-powered car ($2,218).

When comparing cars with a 2024 model year or newer, the cost gap between EVs and gas-powered cars shrinks to 18%, or $501 annually, as advanced technology becomes standard across all vehicles.

Washington, D.C., is the most expensive location for auto insurance for EVs and gas-powered cars. The average annual cost of full coverage there is $6,394 for EVs and $4,124 for gas-powered cars.

Massachusetts, New York, and Rhode Island have the largest cost gap between insuring a newer EV versus a newer gas-powered car. In Massachusetts, it costs 54% more to insure a new EV than a new gas-powered vehicle.

Mercedes-Benz, Tesla, and BMW models top the list of the most expensive EV models to insure.

The 10 states where drivers pay significantly more to insure newer EVs

Auto insurance costs, including for EVs, vary widely by state. Factors like climate risk, vehicle theft rates, population density, insurance regulation, repair infrastructure, and EV adoption levels contribute to regional cost differences. While growing EV adoption can lead to improved infrastructure over time, it can also increase insurers’ exposure, keeping rates elevated even as the market matures.

States with the largest gaps tend to be either dense coastal markets with higher collision and repair costs, or less dense regions where limited service networks and severe weather events drive up risk. Inflation on motor vehicle parts and equipment decreased slightly in April after hitting an all-time high in March, affecting claims costs for EVs and gas-powered cars alike. But thin certified-mechanic ecosystems can increase wait times and lead to higher repair costs.

Insurify ranked states using insurance rate data for newer EVs and gas-powered cars, including model years 2024, 2025, and 2026, to compare more technologically similar vehicles. The average insurance cost gap between these newer models is 18%, according to Insurify data.

1. Massachusetts

Insurance cost difference for EVs vs. gas-powered cars: 54%

Average annual EV insurance premium (newer models): $3,560

Average annual premium for gas-powered cars (newer models): $2,318

Massachusetts is one of the most expensive places to live in the country. While it has a relatively mature EV market, its dense urban exposure, higher-value vehicles, and elevated labor and repair costs for EVs drive up premiums.

“The Boston metro has a high concentration of affluent urban buyers who are early EV adopters, but the body shop network hasn’t kept pace,” said Daniel Lucas, senior carrier partnerships manager at Insurify. “When your car needs a specialist and the nearest qualified shop has a three-week wait, that’s not just an inconvenience — it shows up in your premium.”

Massachusetts also doesn’t allow insurers to use credit history as a rating factor. In another state, a driver with a high-value car and good credit may see lower rates, but in Massachusetts, their strong credit history wouldn’t lower their insurance costs.

2. New York

Insurance cost difference for EVs vs. gas-powered cars: 45%

Average annual EV insurance premium (newer models): $4,531

Average annual premium for gas-powered cars (newer models): $3,135

A few factors drive up EV insurance costs in New York: its high urban claim frequency in the New York City area and its sparse EV repair infrastructure upstate. The New York City, Newark, and New Jersey metro area has the second-highest auto theft volume in the country, according to National Insurance Crime Bureau (NICB) metro crime data shared with Insurify.

It’s also the fifth-most-expensive state for car insurance overall, according to Insurify data.

“New York’s insurance market is expensive by almost every measure, and EVs inherit all of those baseline costs before any EV-specific factors enter the picture,” Lucas said. “EV owners are concentrated in urban corridors where there are also more vehicles and more incidents. Insurers are paying out more and passing along those costs.”

3. Rhode Island

Insurance cost difference for EVs vs. gas-powered cars: 39%

Average annual EV insurance premium (newer models): $6,043

Average annual premium for gas-powered cars (newer models): $4,344

Rhode Island has seen auto insurance premiums skyrocket by 41% since the start of 2024, according to Insurify’s auto report. High population density and urban exposure in a small state have exacerbated premium pressures. Severe weather and coastal flooding also drive up costs; 2024 storms caused flooding that led to an increase in comprehensive claims.

Rhode Island is behind in EV adoption. It’s investing $24 million to install 102 additional EV charging stations across the state and offers rebates for new and used EVs. But its still-maturing EV market is catching up to infrastructure needs.

“You’ve got meaningful adoption relative to the state’s size, but the repair ecosystem hasn’t kept pace,” Lucas said. “So, when a claim drags out, the bill to the insurer grows, driving up premiums.”

4. Oregon

Insurance cost difference for EVs vs. gas-powered cars: 36%

Average annual EV insurance premium (newer models): $3,346

Average annual premium for gas-powered cars (newer models): $2,454

Oregon’s history of strong EV incentives has supported adoption, but its high-risk claims environment has contributed to higher insurance costs for EVs. In 2025, the Portland, Vancouver, and Hillsboro metro area ranked in the top 25 metro areas for auto theft volume, according to the NICB. That represented a 28% drop from 2024, though, so any pressure auto thefts have put on premiums may wane.

Wildfires and subsequent flooding can lead to more comprehensive insurance claims. If thefts or climate damage lead to more expensive claims, drivers can feel that cost in their premiums.

5. New Jersey

Insurance cost difference for EVs vs. gas-powered cars: 36%

Average annual EV insurance premium (newer models): $5,632

Average annual premium for gas-powered cars (newer models): $4,145

New Jersey had 272,376 registered EVs statewide by the end of 2025, not far off from its goal of 330,000, according to the North Jersey Transportation Planning Authority. The state shares some similarities with New York, including having the metro areas with the second-highest volume of auto thefts in 2025, according to the NICB.

Severe weather risk, especially flooding, also drives up comprehensive claims costs for insurers. Just last year, several storms caused flooding that inflicted “significant damage to many homes, businesses, and vehicles,” according to the New Jersey Department of Banking and Insurance.

6. Idaho

Insurance cost difference for EVs vs. gas-powered cars: 31%

Average annual EV insurance premium (newer models): $2,063

Average annual premium for gas-powered cars (newer models): $1,573

Idaho’s EV adoption is growing but still relatively low, at 0.55% in 2024, according to the U.S. Department of Energy (DOE). Limited infrastructure and a sparse repair ecosystem can drive up insurance costs for EVs.

But Idaho is pushing forward with infrastructure development. In November, the Federal Highway Administration approved Idaho’s National Electric Vehicle Infrastructure (NEVI) plans to build a network of charging stations.

Migration from California and Washington, two states with high EV adoption, may explain Idaho’s persistence. Former Washington and California residents accounted for nearly half of Idaho’s migration-related population growth in 2024, according to the American Community Survey.

7. Washington

Insurance cost difference for EVs vs. gas-powered cars: 30%

Average annual EV insurance premium (newer models): $3,260

Average annual premium for gas-powered cars (newer models): $2,515

Washington’s EV market faces many of the same challenges as Oregon’s, with even higher EV adoption rates and elevated theft rates. The Seattle, Tacoma, and Bellevue metro area ranks among the top for vehicle theft volume and rate per 100,000 people, according to the NICB.

Theft can significantly affect insurance costs because it typically results in a total loss for a vehicle, and many newer EVs are costly to replace. For example, the Tesla Model S is among the five most popular EV models in Washington, according to Insurify data. As a luxury model, it has a starting sticker price of $86,630 for a 2026 edition, according to Kelley Blue Book.

8. Delaware

Insurance cost difference for EVs vs. gas-powered cars: 30%

Average annual EV insurance premium (newer models): $4,046

Average annual premium for gas-powered cars (newer models): $3,123

Delaware has set ambitious goals for EV adoption, and it’s paying off. In 2024, EVs represented 12% of all new vehicles sold or leased in Delaware, according to Delaware’s EV Roadmap report. Like Idaho, it’s also using NEVI funds to build out EV infrastructure.

But Delaware is already an expensive state for car insurance, per Insurify data. It’s densely populated and has a high urban exposure, which can increase the likelihood of accidents. More expensive EVs on the road can lead to higher claims costs for insurers and elevated premiums for drivers.

9. North Carolina

Insurance cost difference for EVs vs. gas-powered cars: 28%

Average annual EV insurance premium (newer models): $2,374

Average annual premium for gas-powered cars (newer models): $1,848

Severe weather exposure has contributed to higher EV insurance costs in North Carolina. Hurricanes have caused major flooding in recent years. Hurricanes Helene and Milton caused severe damage in the mountainous western region when they hit in 2024. Flash floods washed away vehicles, leading to expensive comprehensive claims when insurers had to replace them.

North Carolina also implemented new rate-setting legislation in 2025. This legislation increased its minimum liability limits and expanded its inexperienced driver surcharge from three years to eight. The state also saw a 5% overall auto insurance rate increase, all of which can add to EV insurance costs.

10. Kansas

Insurance cost difference for EVs vs. gas-powered cars: 27%

Average annual EV insurance premium (newer models): $3,073

Average annual premium for gas-powered cars (newer models): $2,411

Kansas has a low EV adoption rate of 0.55%, the same as Idaho’s, according to DOE data. Given the low adoption rate, a sparse certified-mechanic ecosystem likely creates a cost gap. EV owners in Kansas have to travel farther or wait longer to get their vehicles repaired following a claim, compounding repair costs. Severe weather, especially hailstorms and tornadoes, drives up comprehensive claims and also contributes to that cost gap.

Other states stand out when comparing insurance costs for all EVs and gas-powered cars

Numerous factors influence car insurance costs for EVs and gas-powered cars, and each state’s regulatory landscape and adoption rate can contribute to significant variability. For example, California is the country’s largest EV market, with an EV adoption rate of 4.1%, according to the DOE.

While premium pressures like wildfire-related comprehensive claim risk, theft exposure, and high-value vehicles are driving up costs, the cost gap between insuring an EV and a gas-powered car in California is 21%, just above the national average, according to Insurify data. The state’s robust adoption means insurers have more EV claims experience, enabling them to accurately price risk.

Washington, D.C., while a much smaller EV market, has an adoption rate of 3.3%, second only to California. It’s also the most expensive location for car insurance, where insurance costs an average of $6,102 per year for new EV models and $4,821 per year for newer gas-powered cars, per Insurify data. It costs 27% more to insure a new EV than a new gas-powered car, according to Insurify data.

The dense urban exposure, high cost of living, and elevated theft and vandalism rates in D.C. have driven up rates for all vehicles. But elevated premiums for gas-powered cars could partially explain the more modest cost gap. Overall, auto insurance costs there went up 18% in 2025, according to Insurify’s auto insurance report.

Michigan presents yet another case: a state with high overall auto insurance premiums but only an 8% cost gap between EV and gas-powered insurance. Michigan’s coverage requirements contribute to high rates across the board. It’s the only state where unlimited personal injury protection remains an option, which can significantly drive up litigation claims costs for insurers regardless of vehicle type.

It’s also one of the few states where the most popular EV isn’t a Tesla — in Michigan, it’s the Chevrolet Equinox, which is much cheaper to insure, per Insurify data. Michigan requires car dealers to obtain a physical commercial location, so Tesla’s direct-to-consumer sales model isn’t legal in the state. Tesla began opening dealerships statewide only in the last few years.

The 5 states where drivers pay the least to insure EVs vs. gas-powered cars

In a handful of states, EVs actually cost nearly the same or are cheaper to insure than gas-powered cars, often because newer gas-powered vehicles are also expensive to insure. These states tend to have smaller EV markets or more balanced risk factors, where vehicle mix and driver profiles can narrow or even reverse the typical cost gap.

1. Montana

Insurance cost difference for EVs vs. gas-powered cars: -4%

Average annual EV insurance premium (newer models): $2,242

Average annual premium for gas-powered cars (newer models): $2,339

Montana’s auto insurance market is low-cost by national standards, mainly due to its low population, low traffic density, and fewer severe weather risks that drive comprehensive claims. Even with low EV adoption and limited EV infrastructure, the modest risks keep premiums lower across the board and lead to similar insurance costs for all vehicles.

“You’ve got a vast geography, low population density, low EV adoption, and a driving culture that’s still overwhelmingly gas-powered,” Lucas said. “Insurers don’t have much EV claim history to work from in Montana, but they also aren’t contending with congested roads. The baseline auto insurance market is less pressurized here, and that carries over to EVs.”

2. West Virginia

Insurance cost difference for EVs vs. gas-powered cars: -4%

Average annual EV insurance premium (newer models): $2,062

Average annual premium for gas-powered cars (newer models): $2,148

West Virginia has one of the lowest EV adoption rates in the country, according to the DOE. It also historically had barriers to EV adoption. The state doesn’t offer rebates to EV owners and charges them a $200 registration surcharge on top of the standard fees. But, like Montana, it’s also a lower-cost state due to less traffic density.

“Because the overall auto insurance market is relatively low-cost, there’s less of a gap to generate in the first place,” Lucas said. “Fewer EVs also mean fewer EV claims, so insurers aren’t under the same pressure as in high-adoption states. The small difference here reflects a market that hasn’t yet been stress-tested.”

3. Nebraska

Insurance cost difference for EVs vs. gas-powered cars: -1%

Average annual EV insurance premium (newer models): $2,055

Average annual premium for gas-powered cars (newer models): $2,086

Nebraska’s low traffic density has helped keep rates low for all vehicles.

“What keeps the EV-to-ICE gap narrow in Nebraska is the same thing that keeps overall auto insurance relatively stable there, lower density, fewer incidents per capita, and a market where insurers aren’t absorbing a disproportionate share of costly EV repairs,” Lucas said. “The infrastructure constraints are real, but they haven’t hit critical mass the way they have in the Northeast.”

Much of the state faces a high hail risk, which can drive comprehensive claims. But many newer EVs and gas-powered vehicles have similar technology, like rain-sensing windshields, which has led to relative cost parity in insuring newer EVs and gas-powered cars.

4. Wisconsin

Insurance cost difference for EVs vs. gas-powered cars 1%

Average annual EV insurance premium (newer models): $1,774

Average annual premium for gas-powered cars (newer models): $1,761

Low baseline premiums and a minimal EV market factor into Wisconsin’s low cost gap between insuring a newer EV and a gas-powered car. Though the state is actively investing in charging infrastructure, a low 0.58% adoption rate means its minimal repair ecosystem hasn’t been tested. And, while the state has some areas of moderately dense urban exposure, much of the state is rural and has low traffic density, leading to lower claims risk.

5. Ohio

Insurance cost difference for EVs vs. gas-powered cars: 2%

Average annual EV insurance premium (newer models): $1,677

Average annual premium for gas-powered cars (newer models): $1,649

Ohio is among the cheapest states for auto insurance, according to Insurify data. While Ohio’s EV adoption rate is relatively low, at 0.67%, and EV infrastructure is relatively limited, Ohio’s lower population density and claims frequency mean insurers aren’t paying out a disproportionate share of EV repair costs. The state, however, is a hotspot for EV manufacturers, which could signal future market growth. As of last July, EV and battery manufacturing created more than 6,000 jobs statewide.

The market influences affecting EV sales

The expiration of the federal EV tax credit significantly affected EV sales, as people rushed to buy one before the credit expired on Sept. 30, 2025.

Sales typically fluctuate from quarter to quarter due to seasonal buying trends. Sales increased by 6% between Q2 and Q3 of 2023 and 4.8% between Q2 and Q3 of 2024, according to Cox Automotive data. Between Q2 and Q3 of 2025, after the announcement that the EV tax credit would be going away, they increased by 40.8%.

But sales dropped dramatically from Q3 to Q4, according to Cox Automotive data. Sales increased by 1.3% during that period in 2023 and 5.6% in 2024, but in 2025 they dropped by 46.5% — even more than they’d increased in the previous quarter.

Though Tesla CEO Elon Musk opposed ending the credit, its expiration seemed to boost Tesla’s market share. Tesla’s market share had dropped to 41% but jumped to 58.9% in Q4 of 2025, Cox Automotive data shows.

Sticker shock at the gas pump could motivate more drivers to jump to an EV, though it remains to be seen whether skyrocketing gas prices will lead to another jump in EV sales.

Gas prices hit an average of $4.24 per gallon in April, according to the U.S. Energy Information Administration. That’s the highest they’ve been since the start of the Ukraine War in 2022, when they hit a record $5.03 per gallon, surpassing the then-record high of $4.11 per gallon from 2008.

The factors contributing to higher insurance costs for EVs

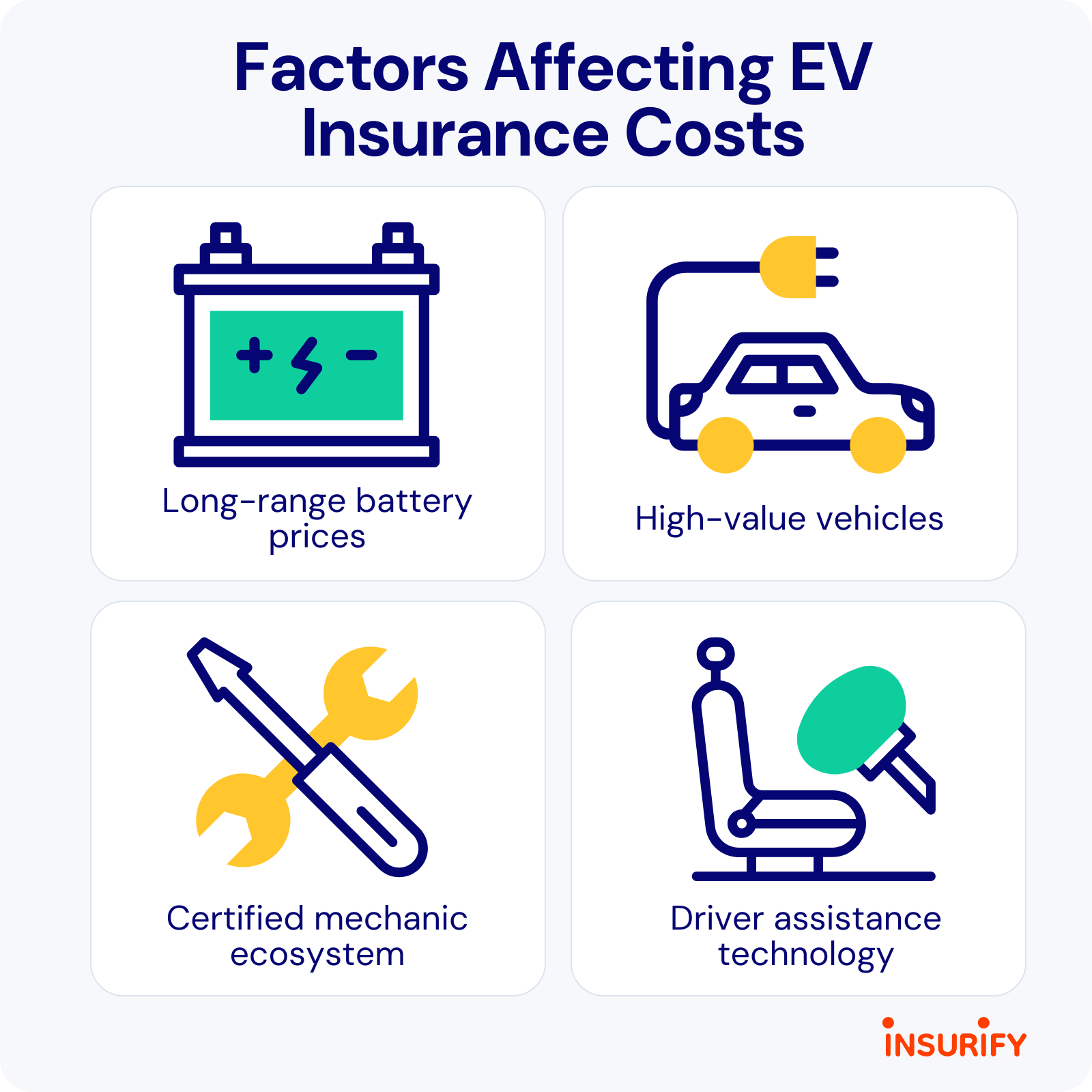

Though newer EVs and gas-powered vehicles are increasingly sharing the same technology, EVs’ need for a long-range battery is still driving higher repair costs. Batteries are still a significant expense in claims calculations, and for good reason: Replacement costs, excluding labor, range from $9,000 to $21,000 for a new battery, according to EV.com.

Chevrolet models have both the lowest and the highest figures: It costs around $9,000 to replace a Bolt battery and $21,000 to replace a Silverado EV battery. Tesla battery replacement costs are consistently in the middle, at around $13,500 for the Model 3 and Y, and up to $15,000 for the Model S and X.

Long-range batteries are becoming less expensive, according to a BloombergNEF analysis. In 2025, lithium-ion battery pack prices fell 8% year over year to $108 per kilowatt-hour. In 2015, the same batteries cost around $500 per kilowatt-hour.

Tariffs have also led to higher claims costs for EVs. Specifically, tariffs on lithium-ion batteries and on graphite, a battery component, from China have significantly increased EV repair costs. Lithium-ion batteries currently face a 25% tariff rate, according to ocean freight company Gateway Lines. Natural graphite from China is subject to a 220% tariff, according to Westwater Resources.

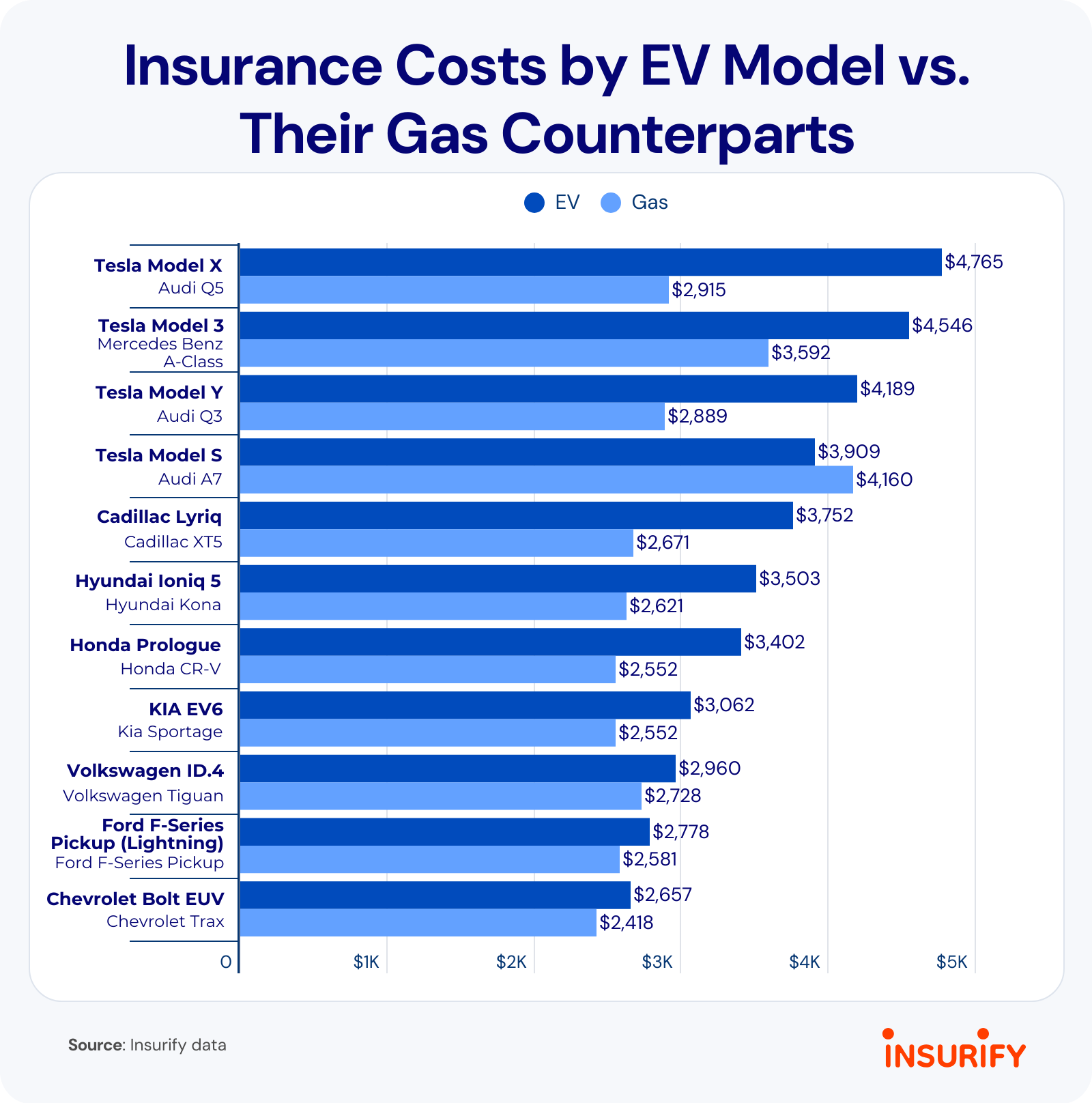

Mercedes-Benz, Tesla, and BMW models top the list of most expensive EVs to insure

Three luxury models, the Mercedes-Benz EQS, Tesla Model S, and BMW i5, top the list of the most expensive EVs to insure, according to Insurify data. All five available Tesla models are among the 10 EVs with the highest insurance costs.

The Tesla Model S is the most expensive Tesla to insure, surpassing the Model X. This is in part due to its high claims frequency: Despite making up just 0.5% of market share, it accounts for 3.97% of repairable battery EV claims, according to Cox Automotive and Mitchell data.

Even the Tesla Model 3 beats out the Model X for insurance costs, Insurify data shows. Its more moderate price point makes it available to a broader range of drivers, but it also has a higher claims frequency relative to its market share.

Despite its high incident rates, Tesla’s Cybertruck is not the most expensive EV or even Tesla model to insure, which speaks to its typical driver profile. It’s such an expensive car that its owners are more likely to have a strong credit history, while other drivers may turn to more affordable models. Still, it’s 50% more costly to insure than the comparable gas-powered truck, Insurify data shows.

Tesla’s “full self-driving (supervised)” technology is also available in most Tesla models. The driver-assistance system may have played a role in multiple vehicle crashes and several fatalities. It’s now the subject of several National Highway Traffic Safety Administration investigations. Despite the system’s name, “full self-driving” is not an autonomous driving program. The system requires the driver to be alert at all times, meaning insurance claims following incidents will affect a driver’s record.

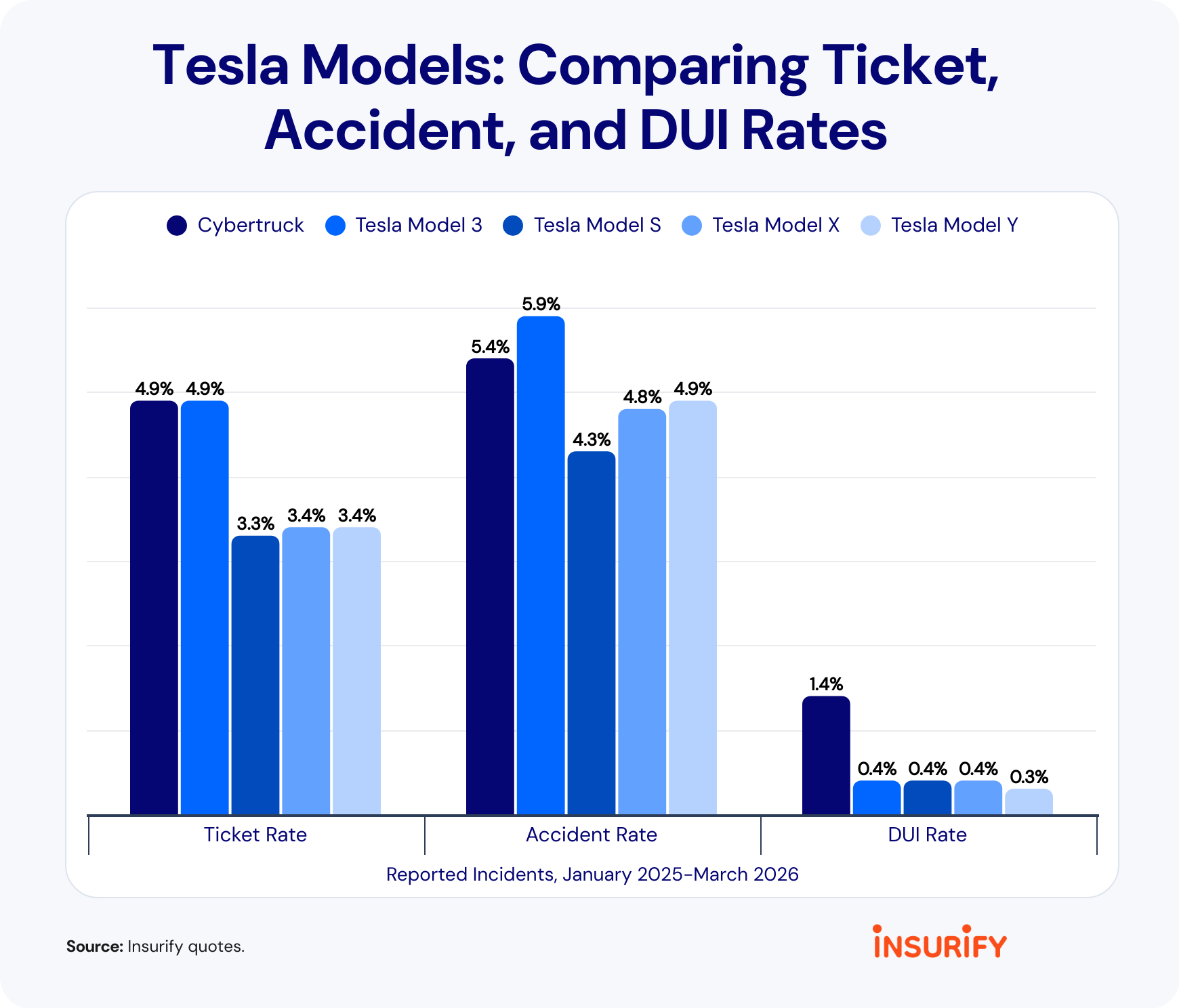

Cybertruck has the highest DUI rate of Tesla models

Insurers factor in driver behavior and claims data when pricing risk, and the car models with the highest incident rates across the board represent different driver cohorts. Muscle cars like the GMC Hummer and Dodge Charger Daytona EV have the highest accident and DUI rates among EV models, Insurify data shows.

Among Tesla models, the Cybertruck has the highest DUI rate, at 1.4%. The Model 3 has a higher accident rate, at 5.9% to the Cybertruck’s 5.4%, Insurify data shows. The Tesla Model 3 has a particularly high repairable claims rate of 25.45% despite its 14.6% market share.

Tips: How to reduce the cost of insuring an EV

EVs often cost more to insure because they’re typically more expensive to repair, require specialized labor, and have pricier parts, though that gap is narrowing as advanced technology becomes standard across all vehicles. Still, personal factors such as driving record and credit history play a major role in premiums, regardless of vehicle type.

For EV drivers looking to minimize insurance costs, shopping around for insurance before deciding on a vehicle can help provide a full picture of EV ownership costs. But drivers who are happy with their current EV still have strategies to lower their premium bill. Maintaining a healthy credit history, considering a higher deductible, and taking advantage of discounts or usage-based insurance policies can all help lower rates.

Methodology

Insurify’s data scientists examined more than 235 million rates in its proprietary database, quoted via integrations with partnering insurance companies, to determine average car insurance rates for gas-powered cars and EVs. Driver applications originate from all 50 states and Washington, D.C., and include information on the exact coverage specifications of each driver’s quoted policies. Insurify excluded Alaska, Hawaii, North Dakota, New Hampshire, South Dakota, Vermont, and Wyoming data due to lower quoting volume.

Full-coverage premiums correspond to policies with bodily injury limits between state-minimum requirements and $50,000 per person, $100,000 per accident; property damage coverage between $10,000 and $50,000; and comprehensive and collision coverage with deductibles of $1,000. Insurify defines “newer” vehicles as models released in the last two years. Rates reflected in the analysis of EVs and comparable models include vehicles of various model years.

Where a manufacturer has an EV and gas-powered version of the same model, like the Ford F-150, Insurify used it as a comparable model. Where this wasn’t the case, Insurify used a gas-powered model from the same manufacturer of the same size class (crossover SUV, midsize sedan, etc.) as an EV to determine a comparable model. For Teslas, Insurify used similarly priced and sized luxury vehicles as the comparison. Unless otherwise specified, the quotes are for a driver with a clean driving record and average or better credit.

To estimate the fuel-cost savings for EV owners, Insurify data scientists compared the annual cost of gasoline to the cost of EV home charging, assuming both vehicles travel 13,482 miles per year. Gasoline costs are based on the U.S. national average price of $4.49 per gallon on May 26, 2026, applied to a vehicle averaging 27.1 mpg. EV charging costs are based on the EIA’s most recent U.S. residential electricity rate available at the time of analysis, 18.83 cents per kilowatt-hour (kWh). This was applied to a vehicle averaging 3.5 miles per kWh.

(0) comments

Welcome to the discussion.

Log In

Keep it Clean. Please avoid obscene, vulgar, lewd, racist or sexually-oriented language.

PLEASE TURN OFF YOUR CAPS LOCK.

Don't Threaten. Threats of harming another person will not be tolerated.

Be Truthful. Don't knowingly lie about anyone or anything.

Be Nice. No racism, sexism or any sort of -ism that is degrading to another person.

Be Proactive. Use the 'Report' link on each comment to let us know of abusive posts.

Share with Us. We'd love to hear eyewitness accounts, the history behind an article.