Mortgage rates are likely to rise in November, as a December cut from the Federal Reserve has started to seem uncertain.

Mortgage interest rates fell ahead of Fed cuts in September and October, because mortgage lenders worked market predictions into their base rates instead of waiting for confirmation. Even though markets are leaning toward a third consecutive cut at the Federal Reserve's Dec. 9-10 meeting, there's enough doubt that staying in wait-and-see mode feels more appropriate.

Anyone hoping we'd see mortgage rates move decisively below 6% will probably be disappointed. But relatively recent home buyers whose mortgages have rates in or near the 7% range will likely still be in a good position to refinance to a lower rate.

Next Fed cut far from guaranteed

Federal Reserve Chair Jerome Powell's Oct. 29 press conference took a bit of a finger-wagging tone as Powell seemingly chastised over-eager prognosticators. "In the committee's discussions at this meeting, there were strongly differing views about how to proceed in December," he noted in his opening remarks. "A further reduction in the policy rate at the December meeting is not a foregone conclusion."

Markets had pretty much decided a 25-basis-point cut in December was a sure thing, so reactions to Powell's comments were swift. Stocks went down, Treasury bonds and mortgage rates — which tend to move together — went up.

There's still enough of a chance for another Fed cut in December that mortgage rates aren't likely to ramp up dramatically this month, but expect higher rates than we saw in October. If inflation appears to be gathering steam, that would make upward movement more decisive. Raising the federal funds rate is the Federal Reserve's method for curbing inflation. Strong enough inflation wouldn't just take a rate cut off the table; it could open up the possibility of a rate hike.

Employment outlook could change

How could this prediction go wrong? Well, a weakening labor market would point to the need for a rate cut. When employers are pulling back, the Federal Reserve lowers rates to ease the cost of borrowing and hopefully get more cash flowing.

With the ongoing government shutdown cutting off access to federal data like the jobs report, data from private firms has helped provide an idea of what's happening in the U.S. economy. The payroll company ADP's employment report has become a stand-in for the jobs report, though it omits public sector workers (and we know layoffs are happening there).

ADP's next report comes out Nov. 5, but preliminary numbers covering through the first two weeks of October showed growth. Assuming that trend continued through the end of the month, that data isn't endorsing a rate cut.

But a few prominent companies announced significant layoffs at the end of October. If those become widespread or have a chilling effect on the stock market, a December rate cut from the Fed would look a lot more likely. And yes, mortgage rates would trend downward.

What other forecasters predict

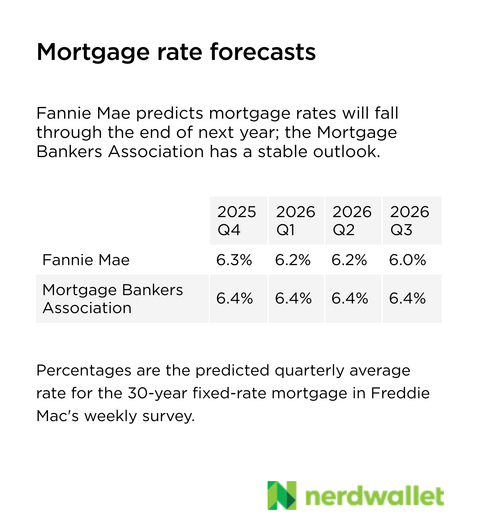

In October, the Mortgage Bankers Association and Fannie Mae both revised their predictions slightly downward for the final three months of 2025 — by 10 basis points, to be precise. The MBA projects this quarter's average rate for 30-year, fixed-rate mortgages will be 6.4%. Fannie Mae has it slightly lower, at 6.3%.

Freddie Mac's weekly mortgage rate survey is averaging 6.3% so far this quarter, but then again, we're only a month in.

What happened in October

Last month, we predicted that mortgage rates would slide downward as the government shutdown created uncertainty both general (when would it end?) and highly specific (key economic data wasn't released). The Federal Reserve's widely anticipated rate cut also fueled downward momentum. And that was pretty much exactly what happened.

More From NerdWallet

The article November Mortgage Outlook: Rates on the Rise originally appeared on NerdWallet.

(0) comments

Welcome to the discussion.

Log In

Keep it Clean. Please avoid obscene, vulgar, lewd, racist or sexually-oriented language.

PLEASE TURN OFF YOUR CAPS LOCK.

Don't Threaten. Threats of harming another person will not be tolerated.

Be Truthful. Don't knowingly lie about anyone or anything.

Be Nice. No racism, sexism or any sort of -ism that is degrading to another person.

Be Proactive. Use the 'Report' link on each comment to let us know of abusive posts.

Share with Us. We'd love to hear eyewitness accounts, the history behind an article.